AI, Data 8 min read

From credit scoring to GenAI: How modern credit decision-making has evolved—and what’s next

The field of credit decision-making is anything but static. As new technologies emerge, underwriters continuously innovate to enhance critical aspects of the process, from predicting the probability of default to pricing loans and effectively managing customers throughout the loan lifecycle.

Today, Generative AI (GenAI) is transforming credit decision-making with unprecedented speed, and its real-world impacts are only beginning to unfold. In this article, Romain Mazoué, Group Chief Risk Officer at Younited, explores the evolution of credit decision-making, delves into Artificial Intelligence (AI) and GenAI use cases shaping the industry, and provides a glimpse into the future as these technologies become integral to lenders’ operations.

Key takeaways

- From manual to automated credit decision-making: Over decades, credit decisions have evolved from manual processes reliant on human judgment to highly automated, data-driven systems powered by AI and machine learning (ML).

- Leveraging diverse data for better outcomes: With AI and ML and broader data availability, lenders can now analyze vast amounts of both traditional and non-traditional data—such as social media activity and utility payments—unlocking more nuanced and personalized credit assessments.

- GenAI enhancing decision-making capabilities: Generative AI adds a new layer of sophistication by interpreting unstructured data, generating insights, and enabling human-like interactions, further advancing the capabilities of AI and ML in credit decision-making.

- Addressing challenges for sustainable adoption: Despite its potential, widespread adoption of GenAI requires financial institutions to mitigate risks related to bias, governance, and system reliability to ensure fair and ethical applications.

- Shaping the future of customer-centric lending: By integrating GenAI responsibly, lenders can streamline credit decision-making while fostering innovation, inclusivity, and efficiency, redefining industry standards for customer-focused financial services.

A short history of credit decision-making

The credit underwriting process has evolved significantly over time, from manual, subjective evaluations to highly automated and data-driven systems. Below is a detailed chronology of the decision-making system for credit underwriting:

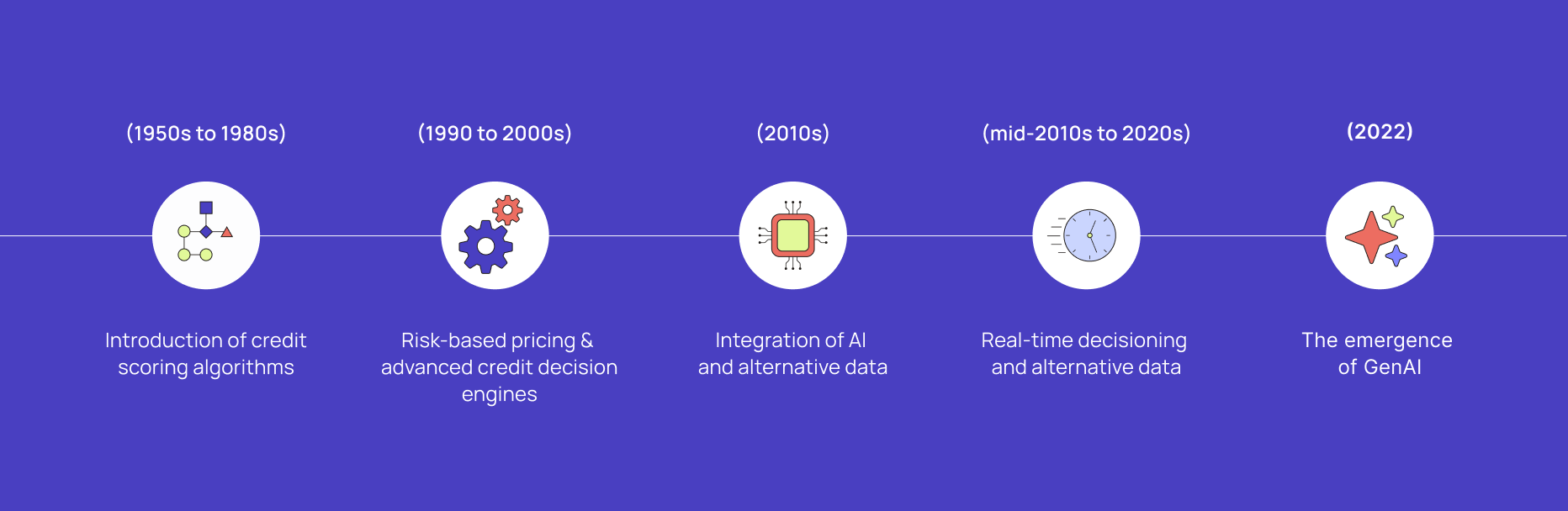

1. Introduction of credit scoring algorithms (1950s to 1980s)

Manual Underwriting & expert judgment

In the early days of credit underwriting, decisions were made manually by credit managers or underwriters. These individuals would review an applicant's financial information, such as income, debts, and personal characteristics, to assess their creditworthiness. The process was highly subjective, potentially influenced by biases such as race, gender, or personal judgments about an applicant's character. This manual approach was time-consuming and prone to inconsistencies.

Introduction of credit scoring algorithms

The first major shift in credit underwriting came with the development of credit scoring models in the 1950s. FICO (Fair Isaac Corporation), founded in 1956 by Bill Fair and Earl Isaac, introduced one of the first credit score models for lenders. These early models were designed for specific businesses and were not universally applicable across different industries. Three other main players in the credit scoring field were also created during this period.

- Experian: The company was founded in 1980 as CCN Systems in Nottingham, England. The U.S. branch of Experian traces its roots back to 1897 when Jim Chilton created the Merchants Credit Association.

- Equifax: Originally founded as the Retail Credit Company in 1899 by Cator and Guy Woolford in Atlanta, Georgia. The company changed its name to Equifax in 1979.

- TransUnion: Established in 1968 as a parent holding company for the Union Tank Car Company. In 1969, TransUnion acquired the Credit Bureau of Cook County, marking its entry into the credit reporting industry.

In the 70’s, the Fair Credit Reporting Act (FCRA) started to regulate the collection of personal credit information and customers’ access to credit reports in the USA.

By the 1980s, credit bureaus began to digitize consumer data, and credit scoring algorithms became more widely adopted. In 1989, FICO released its first "universal" credit score model that could be used by any lender through credit reporting agencies such as Equifax, Experian or TransUnion. This marked the beginning of a more standardized and objective approach to assessing credit risk

At this time, fixed pricing was the norm despite significant differences in customer costs (specifically cost of risk), with loan APR only being changed by expert judgment.

2. Risk-based pricing & advanced credit decision engines (1990 to 2000s)

Broader usage of credit score

In the 1990s, more complex underwriting systems began to emerge, initially with credit card products, before gaining significant traction across other lending products, particularly in the mortgage industry. Pioneered by US government-sponsored enterprises like Fannie Mae and Freddie Mac, these systems aimed to streamline the underwriting process by automating the evaluation of borrower creditworthiness based on predefined criteria such as credit scores and debt-to-income ratios. These new underwriting systems significantly reduced the time required for loan approvals and improved consistency in decision-making.

In the early 2000s, advancements in computing power and data analytics led to the development of more sophisticated statistical models, such as logistic regression, to predict default risk more accurately. Banks began hiring data scientists and statisticians to develop these models, which were trained on large datasets containing hundreds of variables related to borrower behavior. Credit decision engines gradually became integral to financial institutions' tech stacks, enabling real-time decision-making based on a wide range of borrower data.

In parallel, multiple events contributed to fostering wider usage of credit scoring and an improvement in loan pricing:

1. US regulation & credit scoring availability

The US Congress passed the Fair and Accurate Credit Transaction Act in 2003. The act allowed consumers to request and obtain a free credit report once every 12 months from each of the three nationwide consumer credit reporting companies (Equifax, Experian, and TransUnion). However, the adoption of this was slow due to the lack of marketing and consumer awareness.

2. Basel II Regulation

The Basel II Internal Ratings-Based Approach (IRBA) requirements were officially released in June 2004. This framework allowed banks to use their own internal ratings to assess credit risk and calculate regulatory capital requirements, provided they met certain minimum conditions and received approval from their national supervisors.

By allowing banks to develop and use their own models, the IRBA incentivized institutions to improve their risk management practices. Banks were encouraged to adopt more sophisticated modeling techniques to better assess and manage their credit risk exposures through risk parameters estimation. These models allowed for a more dynamic assessment of credit risk, incorporating both observable and unobservable risk factors.

The IRBA introduced stringent regulatory requirements for model validation and approval. Banks had to demonstrate that their internal models were robust, accurate, and consistent with regulatory standards. This led to increased scrutiny of modeling practices and encouraged continuous improvement in model development and validation processes.

3. Capital One & risk-based pricing

Early innovators went beyond credit scoring to undertake sophisticated modeling of multiple additional factors, including churn, marketing efficiency, customer lifetime value, and profitability scoring.

In the 1990s, Capital One developed an innovative targeted marketing approach, focusing on customer profitability analysis, to achieve remarkable success as a leading credit card issuer. It maintained its competitive edge by investing in infrastructure and personnel and continually enhancing its expertise through a 'test-and-learn' methodology. Capital One’s “information-based” strategy consisted of deploying an advanced risk-based pricing approach.

3. Integration of AI and alternative data (2010s)

The next leap in credit underwriting came with the integration of Artificial Intelligence (AI) and Machine Learning (ML) technologies. These tools allowed lenders to analyze vast amounts of both traditional and non-traditional data (e.g., social media activity or utility payments) to make more nuanced credit decisions.

AI-driven systems could assess borrower reliability beyond conventional metrics like credit scores, broadening access to credit for individuals with limited credit histories. AI also improved risk assessment by identifying patterns in borrower behavior that traditional models might miss. However, several challenges appeared with the new generation of models, specifically the lack of transparency and the potential risk of model biases leading to discrimination.

The growing usage of alternative data has fueled the emergence of AI models. By better leveraging large datasets of non-linearly correlated and diverse data, AI models have shown their superiority to traditional statistical models. For credit decision-making, alternative data usually include (i) open banking data, (ii) utilities and rental payment history, (iii) open admin data, and (iv) digital footprint. This approach has proven particularly beneficial for underserved populations, such as recent immigrants or gig economy workers, who might otherwise be excluded from traditional lending systems.

4. Real-time decision-making and alternative data (mid-2010s to 2020s)

Today, many lenders use real-time data analytics to make instant decisions on loan applications. Automated systems can now integrate alternative data sources—such as rental payment history or utility bills—to assess borrowers who might not have a robust credit history. This shift has made lending more inclusive while maintaining rigorous risk management practices.

Additionally, modern decision-making systems now allow for greater agility in decision-making through configurable rules that can be adjusted without extensive reprogramming. SaaS decision-making platforms, for instance, enable lenders to design and test highly segmented, real-time decision workflows and models tailored to their customer base.

5. The emergence of GenAI (2022)

While AI models have existed for decades—dating back to the 1980s with logistic regressions—they were limited by smaller datasets and less computational power. In contrast, the foundations of GenAI models are relatively recent, beginning with the development of Transformer models by Google in 2017 and the release of BERT in 2018. BERT marked a breakthrough in language processing, revolutionizing the ability to understand context through its transformer-based architecture

In November 2022, OpenAI released ChatGPT, which quickly became a groundbreaking product due to its ability to generate human-like text. Within two months, it gained over 100 million users, making it the fastest-growing consumer application in history. Two years later, GenAI models have continued to improve, with multiple new major players competing with ChatGPT: Gemini, Android, and Mistral, for example.

Over the past two years, the performance of LLM models has improved at a fast pace, with the following noticeable evolutions:

- Multimodal capabilities in models have expanded their functionality beyond text generation to include image and code generation, broadening their application scope.

- Performance optimization and model customization through RAG, fine-tuning, and prompt engineering have gained in maturity.

- There is now stronger integration of GenAI agents in most software solutions via chatbot, copilot, and others.

- The efficiency and scalability of generative AI models have improved, enabling them to handle larger workloads and provide faster responses, allowing real-time interactions.

- Smaller or open-source versions of GenAI models have improved portability and cost efficiency.

Additionally, hardware capabilities have followed the Gen AI hype, with Nvidia becoming the largest corporate valuation in the world—going from $500 billion to $3,200 billion!

These examples illustrate how fast GenAI has moved from a novel technology to a widely adopted tool across various industries, enhancing efficiency and personalization in numerous applications.

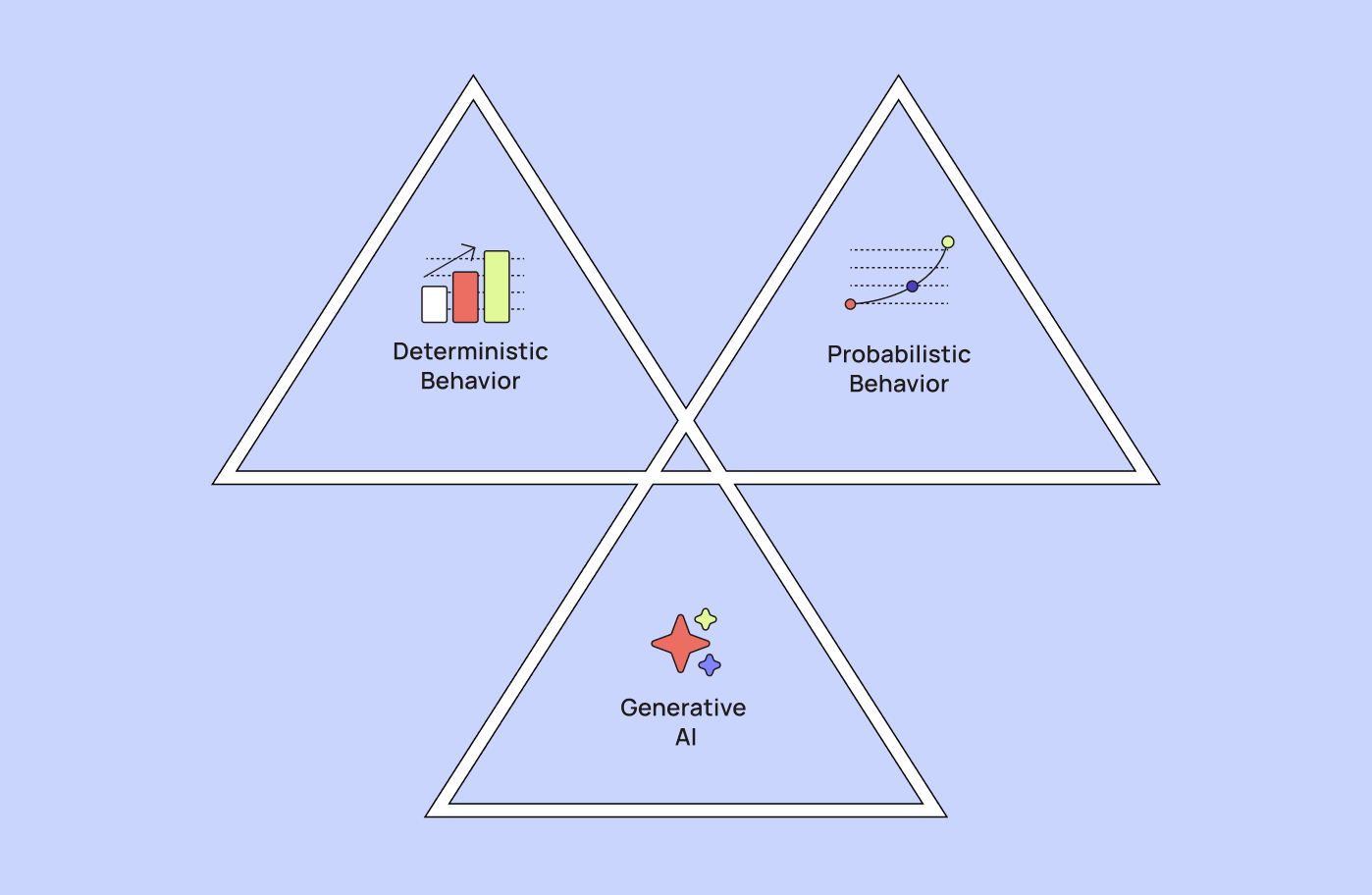

Over the past years, structural trends have reshaped how credit decisions are processed through three phases. We first shifted from deterministic behavior based on expert rules to probabilistic behavior with machine learning and deep learning models, which can learn from data without being explicitly programmed. Then, the third phase is the GenAI models that use content to create new content and process complex workflows. These three generations of models can be used together in a complementary way.

Another noticeable trend is the switch from proprietary software such as SPSS or SAS to open-source tools and libraries (R, python). The open-source community has fostered innovation and continuous improvement by making new tools and algorithms, such as XG Boost or CAR, available.

AI and GenAI use cases for credit decision-making

Zooming in on the second and third phases mentioned above, in the context of credit decision-making and loan applications, AI and Generative AI (GenAI) offer distinct capabilities that complement each other to enhance the loan approval process.

AI capabilities in credit decision-making

Traditional AI models think as a deductive brain to make decisions. They can be used in multiple steps of a credit decision-making framework, for example:

- Predictive analytics and risk assessment: AI leverages predictive analytics to assess creditworthiness by analyzing vast datasets, including financial behavior and spending patterns based on open banking. This enables lenders to make informed decisions quickly and reduce the risk of defaults. They can identify nonlinear relationships and complex interactions within a vast amount of data that logistic regression might miss.

- Fraud detection: AI excels in identifying suspicious patterns and anomalies in real time, which helps in preventing fraudulent activities before they impact financial institutions.

- Automation and efficiency: AI models can help automate repetitive tasks such as data entry and compliance checks, improving processing times and reducing human error. This leads to faster loan approvals and enhances operational efficiency. Additionally, AI models can automate the model development process itself with automated feature selection and model selection, reducing the need for manual intervention.

GenAI capabilities in credit decision-making

GenAI models work similarly to the inductive brain, as they can demonstrate creativity and problem-solving approaches. The new set of capabilities brought by GenAI models can be summarized as follows:

- Comprehend: Process into meaning, reverse engineering, and problem-solving.

- Converse: Human-like dialog, natural language interaction, and instruction.

- Create: Writing, images, code, and multimodal content generation.

- Coach: Real-time coaching.

- Command: Determination of best workflows.

While this new set of new capabilities is generic, we see more and more examples of successful Gen AI implementations to tackle risk management topics:

- Product development: GenAI-enabled programming, code testing, code documentation generation, and identification of trends to drive new product development.

- Sales & distribution: Customer segmentation and sentiment analysis, hyper-personalized offers, content generation, and pricing optimization.

- Operations: Onboarding, credit scoring, servicing, collections, and enhanced underwriting.

- Risk & compliance: Risk monitoring and early warnings, suspicious activity report generation, contract monitoring, fraud and money laundering prevention and detection, document summary for credit underwriting, proactive recovery actions, and risk and compliance knowledge management – all of which fall within the focus of this article.

- Support function: Employee self service, knowledge smart search, and document generation.

- Document handling: Processing unstructured data, such as customer feedback or complex financial documents, by summarizing content, extracting key information, and automating document generation. This capability streamlines the credit decision-making process by reducing manual effort and errors.

- Personalization and customer interaction: Enhancing customer service through personalized interactions via chatbots, offering 24/7 support and tailored recommendations. GenAI can also generate personalized repayment plans based on a borrower’s financial history.

AI versus GenAI

There are multiple domains where both types of AI complement each other, such as recommendation engines and demand forecasting. Importantly, GenAI will complement traditional AI opportunities, not replace them!

In summary, while traditional AI focuses on predictive analytics, fraud detection, and automation to streamline credit decision-making processes, GenAI brings advanced capabilities in handling unstructured data, enhancing personalization, and generating synthetic data for model training.

These complementary technologies enable more accurate, efficient, and customer-centric lending practices.

What’s next for credit decision-making in the age of GenAI?

Model risk

Model risk is perhaps the flipside of increasing sophistication and the growing complexity of credit decision-making models with more parameters. Challenges such as lack of transparency, the risk of discriminatory bias, sensitivity to data quality, and limited explainability become more pronounced, posing significant concerns—particularly in the highly regulated financial industry.

AI Act and other regulations

The European Union's Artificial Intelligence Act (AIA) has significant implications for credit decision-making models, as it classifies AI systems used for credit scoring and creditworthiness assessments as "high-risk." The AIA imposes stringent requirements on these high-risk systems, including robust risk management, transparency, accuracy, human oversight, and measures to prevent discrimination or unfair outcomes. These rules aim to mitigate potential risks like bias or lack of interpretability while ensuring that AI-driven credit models operate responsibly.

By fostering accountability and fairness, the AIA seeks to balance the benefits of AI - such as improved efficiency and inclusivity - with the protection of fundamental rights and consumer trust in financial decision-making processes. However, this may also pose challenges for European model developers as compliance challenges and cost might hinder innovation and model performance.

Stronger reliability for GenAI models

GenAI models are known to sometimes provide unexpected outcomes. For highly regulated and sensitive processes such as credit decision-making, this limitation can represent a challenging roadblock. Innovations such as Retrieval-Augmented Generation (RAG) could address challenges like hallucinations, ensuring that AI-generated outputs are grounded in factual data. Moreover, GenAI's ability to generate transparent explanations for decisions could improve trust among consumers and regulators while providing rejected applicants with more humanistic feedback.

Wider adoption and impact on credit decision-making processes

As open finance expands, GenAI will play a pivotal role in integrating data from multiple financial institutions to provide comprehensive credit assessments. With improved reliability and gradual adaptations in internal workflows and software to accommodate this new generation of models, we anticipate significant transformations in operational processes. GenAI models and agents will become increasingly autonomous in the credit decision-making process through the possibility of dynamically managed safety nets triggered by human-in-the-loop checks or controls.

GenAI-based credit decision-making could lead to more accurate and inclusive lending decisions, expanding access to credit for underserved populations while reducing default risks. However, widespread adoption will require financial institutions to address risks related to bias, governance, and system reliability.GenAI models have the power to not only streamline credit decision-making but also foster innovation, inclusivity, and efficiency in the financial sector, setting new standards for customer-centric lending practices.

Disclaimer

This information provided in this article does not, and is not intended to constitute professional advice; instead, all information, content, and material are for general informational and educational purposes only. Accordingly, before taking any actions based upon such information, we encourage you to consult with the appropriate professionals.

Frequently Asked Questions (FAQs)

Q: How has credit decision-making evolved over time?

A: Credit decision-making has shifted from manual underwriting and credit scores to AI-driven credit models that leverage alternative data. Today, lenders are adopting Generative AI (GenAI) to interpret unstructured data and improve credit decisions.

Q: What role does AI play in credit decision-making?

A: AI helps lenders assess credit risk more accurately by analyzing large datasets, detecting fraud in real time, and automating compliance checks. This enables faster loan approvals, reduced default rates, and better customer experiences.

Q: How is GenAI changing credit scoring?

A: GenAI goes beyond predictive analytics by interpreting documents, summarizing complex financial data, and creating personalized borrower interactions. This is helping lenders make more more transparent, inclusive, and customer-centric credit decisions.

Q: What is the future of credit decision-making with GenAI?

A: The future lies in combining AI and GenAI to enable real-time, explainable, and highly personalized credit assessments. With regulations like the EU AI Act shaping adoption, responsible use will be key to remaining compliant while enhancing decision-making. Request a demo to learn how to leverage GenAI in your decision-making strategies.